日本法人から米国法人へのインバージョン実施時における日本税務上の留意点

Attorney admitted in Japan, Japanese Certified Public Tax Accountant

Kenjiro Sano

J-KISS is a simplified funding method using stock acquisition rights, mainly used for seed-stage funding. While it has been about 10 years since its release and its adoption has progressed, there are complex aspects to its mechanism, and it's important to utilize it with a thorough understanding. In April 2022, Coral Capital, which designs and publishes J-KISS, released an updated version ("J-KISS 2.0"). This article will explain the mechanism of J-KISS and key points for its utilization, while also mentioning the differences between the conventional J-KISS and the new J-KISS, as well as points to note.

目次

J-KISS is a format (template) published in 2016 by 500 Startups Japan (the predecessor of Coral Capital) as a simplified funding method for seed-stage startups. It was created with reference to "KISS," which is widely used in the U.S.

The basic concept of J-KISS is to complete funding quickly using a simplified format by postponing the determination of specific conditions. First, funding is implemented and stock acquisition rights are issued by deciding only the investment amount and a few variables. When the stock acquisition rights are converted to shares, the stock price, number of shares issued, shares to be issued (preferred shares), and other contractual rights of investors are determined in accordance with the investment conditions of the next round. Also, elements other than the basic concept are incorporated to protect investors' rights and interests and respond to other scenarios. This mechanism is also common with convertible bonds (CB).

Two points often mentioned as benefits of funding through J-KISS are (1) the realization of simple and quick funding and (2) the postponement of valuation . Specifically, they are as follows:

In J-KISS, the package of investment contracts and content of stock acquisition rights (terms of issuance) is published and widely shared as a format (template). By negotiating between startups and investors, focusing on key conditions based on this, funding can be carried out simply and quickly.

In particular, there is a big difference compared to contract negotiations for funding using preferred shares, and time and costs can be saved (investors can expect the conversion to preferred shares in the next round, as we will see later).

In J-KISS, since the number of shares to be converted is determined based on the valuation of the next round, it can postpone the confirmation of valuation until the next round.

However, the effect of postponing valuation (especially whether a postponement that benefits the startup side can be expected) depends on the design of J-KISS (setting of valuation cap, etc.). In fact, many cases, startups use it without expecting the benefit of postponing valuation determination.

This point will be organized again in 4(3) below.

Next, we will explain the mechanism of J-KISS in detail. Here, we will look at three points: (1) when J-KISS (stock acquisition rights) is converted to shares (conversion events), (2) how the type and number of shares to be converted are determined, and (3) how it is handled in the event of an acquisition.

In the following, we will refer to the company raising funds through J-KISS as the "issuing company" and the investing investor as the "investor" or "J-KISS investor".

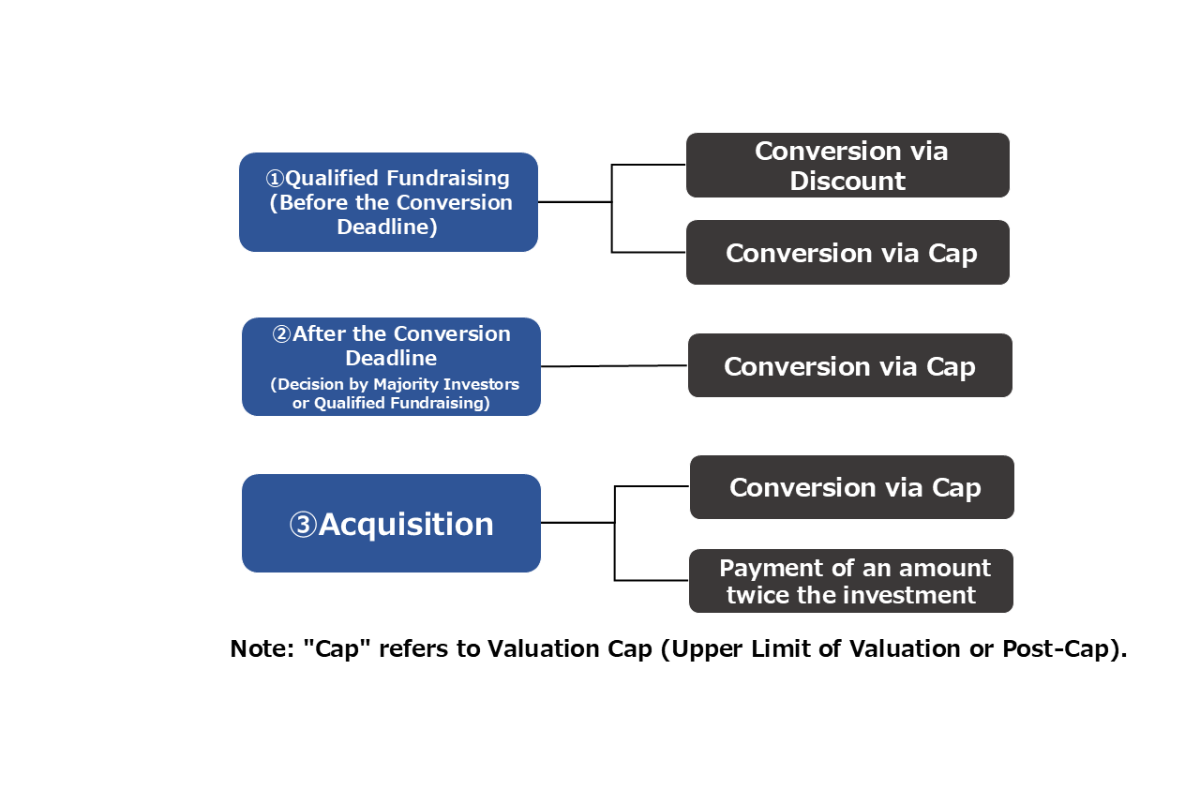

In J-KISS, three events are specified as triggers for conversion to shares (conversion events).

When a funding round of a certain amount or more through shares occurs, J-KISS (stock acquisition rights) is converted to shares. In practice, it is common to have investors exercise their stock acquisition rights, but even if they are not exercised, there is a mechanism for mandatory conversion. The "certain amount" can be set arbitrarily, but many cases set it at "100 million yen or more" aiming for conversion at Series A.

While the J-KISS format uses the term "next funding round", we will use "qualified financing" below to clarify that there are requirements for the amount and method of funding (i.e., it is not necessarily the next funding round).

When the deadline set as the conversion deadline passes, investors can convert J-KISS to shares without waiting for other conversion events to occur. This provides an option for investors to convert to shares at their discretion if qualified financing does not occur within a certain period, aiming to protect investors.

However, conversion to shares requires approval from a majority of J-KISS investors based on the investment amount.

The conversion deadline can be set arbitrarily, but many examples set it at "18 months".

When the issuing company decides to accept an acquisition, investors can convert J-KISS to shares (more precisely, after the conversion deadline, conversion needs to be done through the procedure in (b)). However, investors can also choose to receive twice the amount of their investment in cash instead of converting to shares.

This point will be explained again in (3) "Handling at the Time of Acquisition".

The conversion mechanism of J-KISS differs between conversion due to qualified financing (occurring before the conversion deadline) and conversion due to other reasons. We will first explain the most common conversion due to qualified financing (before the conversion deadline), and then supplement for other reasons.

In case of conversion due to qualified financing, the shares to be issued will be the same type of preferred shares as those issued at the time of qualified financing. However, since the issue price of shares through qualified financing and the issue price through conversion are different, adjustments are made for matters that should be determined based on the share price (such as the preferred distribution amount of residual assets). As a result, it is common for two types of preferred shares to be issued (e.g., Series A1 and Series A2).

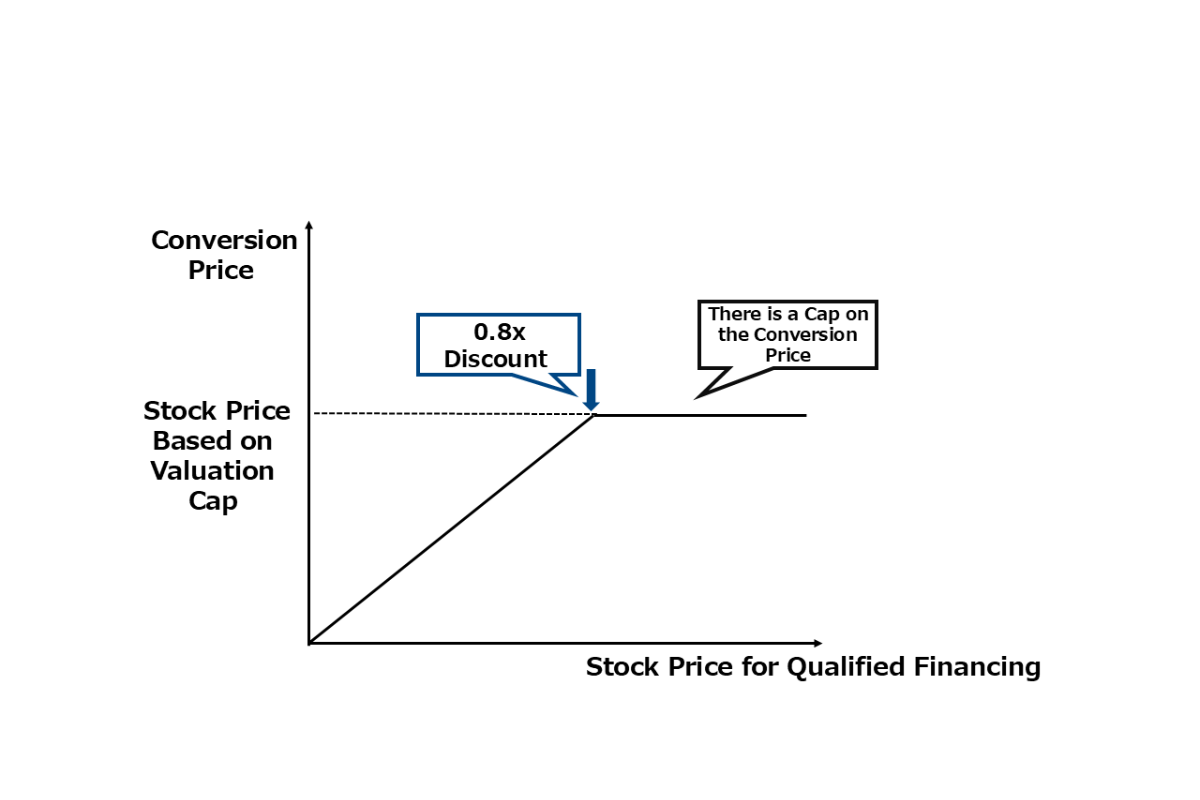

The share price and the number of shares to be issued through conversion accompanying qualified financing are determined by mechanisms called "discount" and "valuation cap" (only when it occurs before the conversion deadline). Specifically, they are as follows:

Discount refers to the discount rate indicating how much cheaper shares can be acquired compared to the issuance conditions in qualified financing.

The acquisition price of shares by J-KISS investors ("conversion price") is determined by applying a certain discount rate to the share price in qualified financing. As J-KISS investors, they can receive the benefit of the discount for investing ahead of qualified financing.

The discount rate can be set arbitrarily, but setting it at "0.8 times" is common.

A valuation cap is a mechanism that sets a certain upper limit on the acquisition price of shares by J-KISS investors ("conversion price"). This ensures that J-KISS investors can acquire shares at or below a certain price regardless of the share price at the time of qualified financing (this means that there is a limit to the "valuation postponement effect" of J-KISS).

As a calculation method, the upper limit of the conversion price is set by dividing the valuation cap by the "fully diluted number of shares" immediately before the qualified financing. If the conversion price calculated based on the discount exceeds this, the number of shares to be issued is determined using this upper limit as the conversion price.

The "fully diluted number of shares" refers to the total number of issued shares and shares converted from stock acquisition rights, but there is an important difference between the conventional J-KISS and the new J-KISS. While the conventional J-KISS does not include J-KISS-type stock acquisition rights, the new J-KISS includes them (note that the new version also includes planned stock options, the so-called SO pool).

In the conventional version, since J-KISS-type stock acquisition rights are not included in calculating the conversion price, the valuation cap becomes the "upper limit of valuation not incorporating the investment amount through J-KISS (= pre-money valuation)". On the other hand, in the new version, since J-KISS-type stock acquisition rights are included, it means the "upper limit of valuation incorporating the investment amount through J-KISS (= post-money valuation)".

The impact of this difference between the conventional and new versions is not limited to the technical point of which time point to use as the basis for defining the "valuation cap". This point will be explained again in 4(d) below.

For reasons other than qualified financing ("expiration of conversion deadline" and "occurrence of acquisition"), the shares issued through conversion will be common shares. On the other hand, in the case of conversion accompanying qualified financing that occurs after the conversion deadline, they will be preferred shares substantially the same as those issued at the time of qualified financing.

The share price and number of shares to be issued through conversion are calculated based on the valuation cap in all cases, including qualified financing after the conversion deadline.

It's a point for investors to be cautious about as the conversion based on the valuation cap becomes fixed if qualified financing does not occur within the conversion deadline.

When the issuing company decides to accept an acquisition by a third party, investors have two options. The first is to participate in the acquisition after converting to shares (common shares) based on the valuation cap. The second is to receive twice the amount of their investment in cash from the issuing company in exchange for the stock acquisition rights, based on the "acquisition clause" of the stock acquisition rights without converting. Investors will choose the option that provides a larger return based on the acquisition amount.

The mechanism allowing receipt of twice the investment amount in cash is in place because there is a risk that sufficient returns cannot be secured (or unexpected losses may occur) through participation in the acquisition by converting J-KISS if the issuing company decides to accept an acquisition at a not very high valuation. In the design of J-KISS, investors do not have the right to stop the issuing company's decision on acquisition, so this mechanism can be said to provide a certain level of investor protection.

As mentioned earlier, conversion in case of a decision to accept an acquisition after the conversion deadline needs to follow the rules for conversion after the deadline, requiring consent from a majority of J-KISS investors.

The basic mechanism of J-KISS is as described above. The scenarios expected after J-KISS issuance can be summarized as shown in the figure below.

Finally, from the perspective of startups, we will introduce the key points and considerations for utilizing J-KISS.

The J-KISS format is designed to focus negotiations between the parties on a few specific terms (variables). To summarize, the negotiable variables are as follows:

- The funding amount threshold for qualified financing (typically 100 million yen)

- Discount rate (typically 0.8x)

- Valuation cap (defined as "valuation cap" in the conventional J-KISS and "post-cap" in the new J-KISS)

- Conversion deadline (typically 18 months)

It should be noted that these variables are not mandatory elements for convertible funding methods like J-KISS. For example, in the U.S., SAFE, which is said to be more widely used than KISS, does not have a conversion deadline. Additionally, in SAFE, the conversion mechanisms of "discount" and "valuation cap" are optional, resulting in four types of formats depending on their inclusion.

In Japan as well, for example, convertible bonds (CBs) offer various variations in their conversion mechanisms. The mechanism assumed in J-KISS should be understood as just one type of convertible funding method in relative terms.

In the standard scenario of conversion through qualified financing, shares substantially identical to those issued in the qualified financing are issued to J-KISS investors.

Qualified financing is generally defined to correspond to Series A funding rounds, such as those exceeding "100 million yen," so it is highly likely that preferred shares will be issued to J-KISS investors.

Preferred shares are associated with various rights, such as liquidation preferences. Additionally, under Japanese corporate law, certain decisions require resolutions by a class shareholders' meeting composed only of shareholders holding the same type of shares, which necessitates attention.

Furthermore, while this article focuses on the aspect of J-KISS's stock acquisition rights, investment agreements concluded at the time of issuance also grant certain rights to J-KISS investors (e.g., preemptive rights).

When considering the use of J-KISS, it is necessary to compare and evaluate these points against other investment methods such as common shares.

As mentioned earlier, J-KISS has the effect of postponing valuation determination until conversion since it does not require setting a share price at the time of funding. However, this effect is limited by the "valuation cap."

To achieve a postponement of valuation that benefits startups, it is necessary to set a sufficiently high "valuation cap." However, in practice, when using J-KISS during the seed stage, it often seems that the "valuation cap" is not set literally as a cap (upper limit), but rather close to the current valuation as assessed by investors. For instance, there are cases where the valuation cap is agreed upon at an amount equivalent to what would be used if equity-based funding were chosen.

In such cases, it is generally expected that conversion will occur based on the valuation cap, making it unlikely that startups will benefit from valuation postponement. On the other hand, investors can hedge downside risks by retaining an option for conversion based on discounts and prevent dilution caused by issuing shares or stock options before conversion (since conversion prices are calculated by dividing the valuation cap by fully diluted shares at the time of conversion).

Additionally, due to J-KISS's design, where conversion based on the valuation cap becomes fixed after the expiration of the conversion deadline or upon acquisition events, there is a structural difficulty for startups in negotiating to raise the valuation cap.

In any case, regarding postponing valuation, achieving this effect is more challenging than generally assumed. If startups aim to utilize J-KISS with this expectation in mind, careful design and negotiation are required.

As explained in 3(2)(a) above, there is a difference in how "valuation cap" is positioned: pre-money valuation in conventional J-KISS versus post-money valuation in new J-KISS.

If this difference were limited to its positioning alone, recognizing and using it with an understanding of what it means—similar to distinguishing between pre-money and post-money valuations in typical funding—would suffice.

However, some caution is needed when conducting multiple rounds of funding through J-KISS (or when such rounds are anticipated). To observe how conversions based on valuation caps differ between conventional and new versions, let us consider a simplified case:

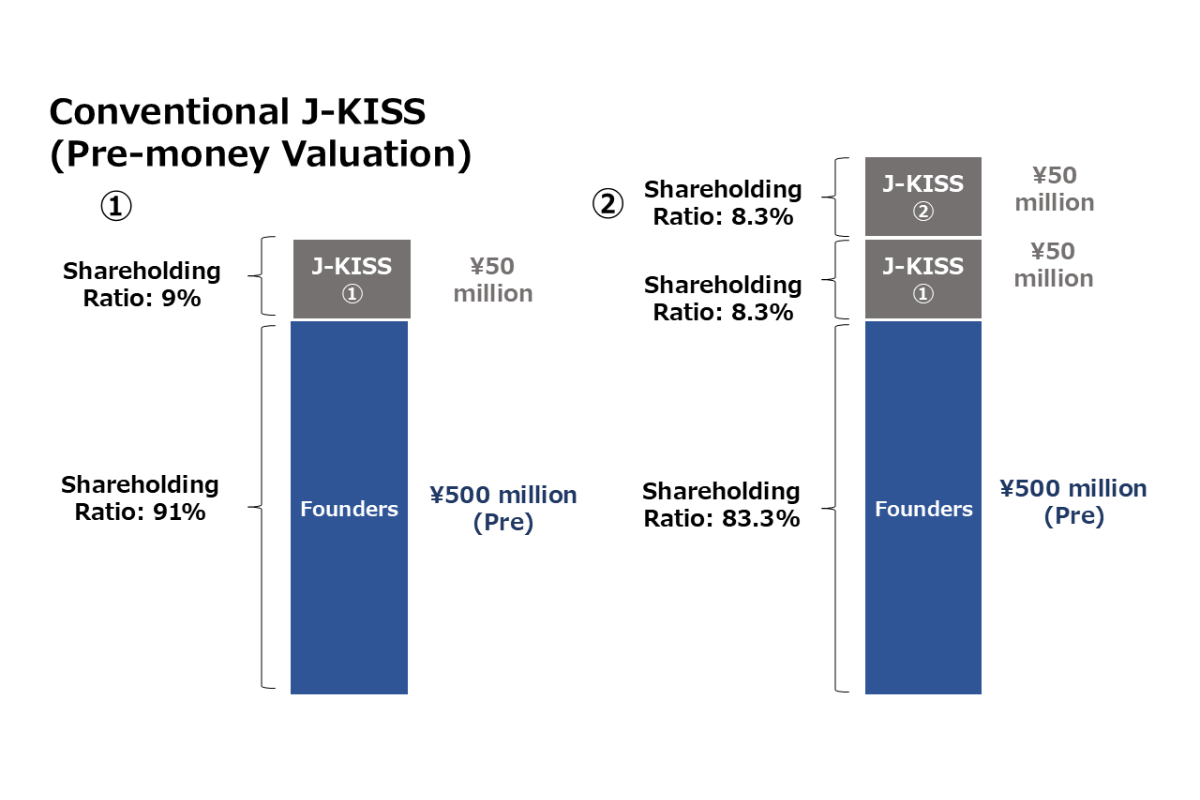

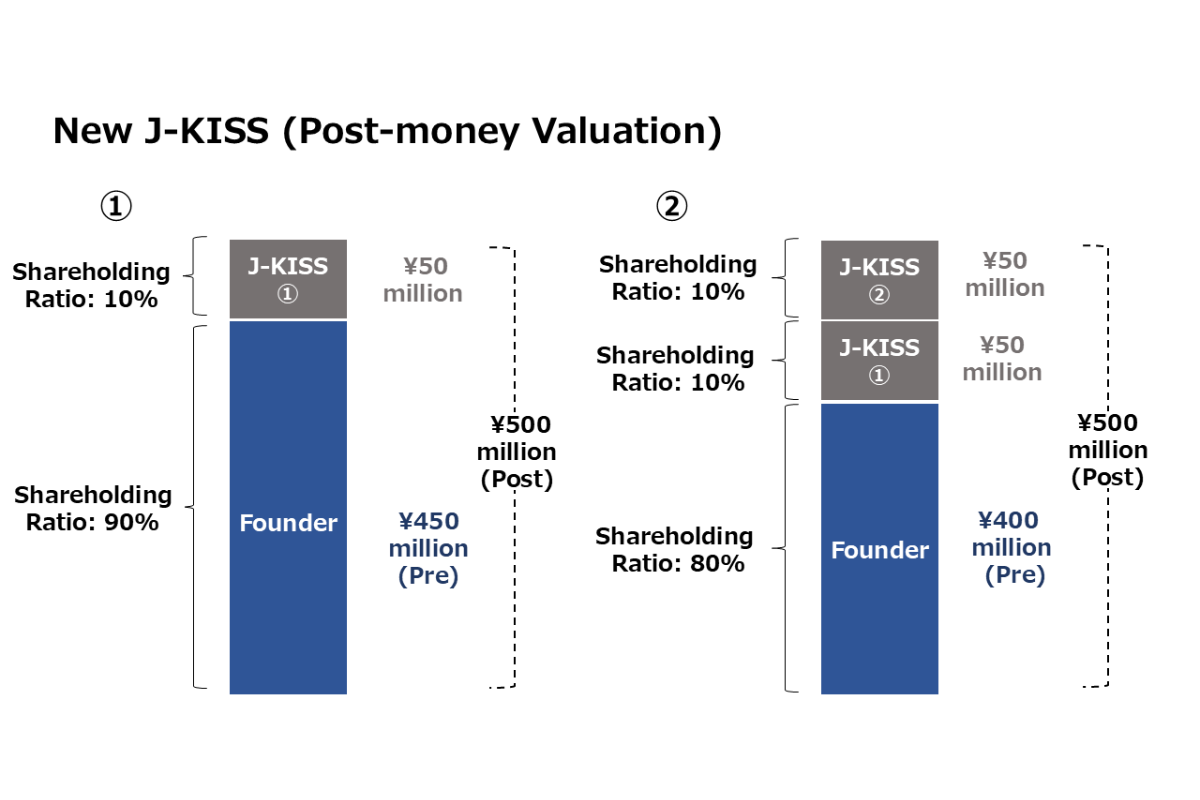

Case 1: When raising 50 million yen through J-KISS with a valuation cap of 500 million yen while founders own 100% equity.

Case 2: After Case 1, raising an additional 50 million yen through J-KISS with the same valuation cap of 500 million yen.

In conventional J-KISS where upper limits are set based on pre-money valuations, even if additional issuances are made with an unchanged valuation cap through subsequent rounds of J-KISS issuance, there is no change to pre-money valuations (i.e., founders’ equity value). In other words, additional issuances do not affect future conversion prices (share prices) based on valuation caps.

On the other hand, in the new version where upper limits are set based on post-money valuations, if additional J-KISS issuances are made under the same conditions, the valuation on a pre-money basis (the value of founders' equity in the figure below) will decrease, resulting in a lower future conversion price (share price) based on the valuation cap.

It can be noted that the new version has the advantage of making it easier to calculate and understand the degree of dilution, as the ownership ratios of each investor after conversion based on the valuation cap are fixed (not affected by additional J-KISS issuances). This advantage is particularly significant in complex cases where J-KISS funding is repeated with changing valuation cap amounts. However, it is crucial to be aware that additional issuances under the same conditions effectively lower the valuation.

J-KISS is a mechanism that allows for rapid fundraising by limiting negotiation points between startups and investors, adhering to published formats, and postponing the determination of certain conditions until the next funding round. As it has become widely adopted in recent years, the effect of simplifying and accelerating fundraising has become significant.

On the other hand, as we have seen, there are many complex points and considerations in the J-KISS mechanism. Therefore, it is necessary to consider its utilization and negotiate conditions with a good understanding of its design and effects. If J-KISS is used without sufficient understanding, it may lead to situations that significantly impact subsequent capital policies.

We hope this article will be helpful for those considering the use of J-KISS to deepen their understanding.

Please let us know if you have further questions or may need assistance on this matter. For further information on the above, about our firm or any other matters, please contact through the form.

Click here for the Japanese original article.

Attorney admitted in Japan, Japanese Certified Public Tax Accountant

Kenjiro Sano

Attorney admitted in Japan

Masayuki Matsunaga

Attorney admitted in Japan, Japanese Certified Public Accountant

Fumihiko Ogata

Attorney admitted in Japan

Masayuki Matsunaga

Attorney admitted in Japan, Japanese Certified Public Accountant

Fumihiko Ogata